In today’s Autumn Statement, Chancellor Jeremy Hunt unveiled 110 measures to boost economic growth ahead of next year’s general election. The statement emphasised the UK’s strong commitment to promoting innovation and research and development (R&D).

An important aspect of this commitment is the planned merger of the R&D tax relief schemes, which is expected to include a significant increase in financial incentives. By the fiscal year 2028-29, an additional £280 million per year is expected to be allocated to R&D relief, establishing the UK as a leading centre for cutting-edge R&D.

These developments have significant implications for businesses engaged in innovative R&D activities. We’ve provided a concise overview of the changes announced today to help you stay informed.

Overview of the R&D Tax Relief Changes

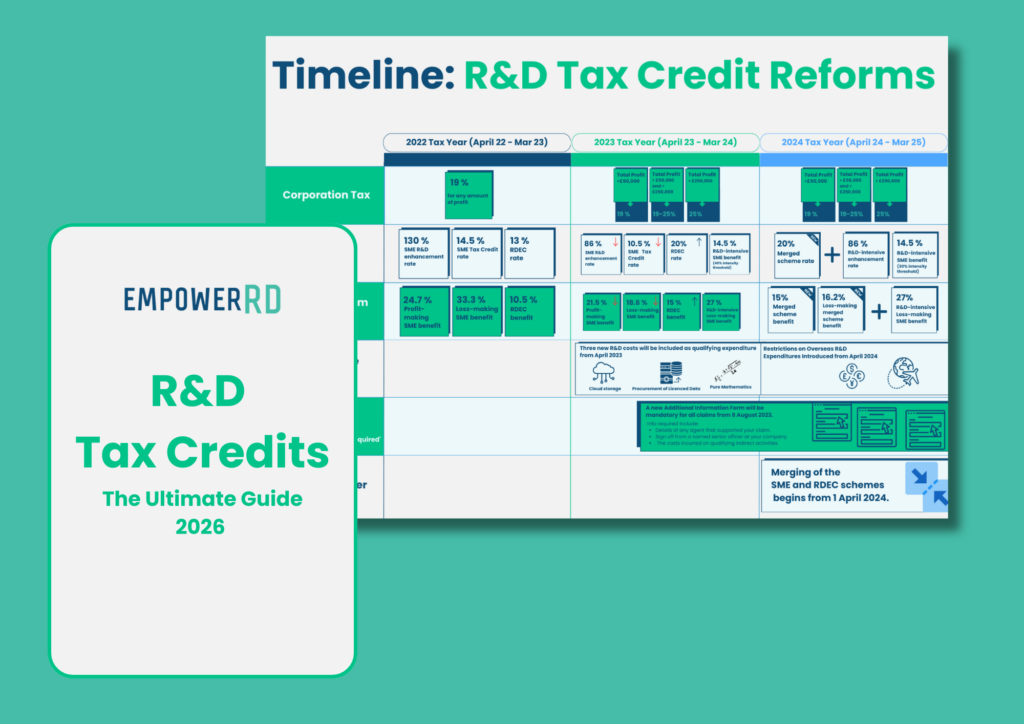

The Autumn Statement for 2023 confirmed reforms to the R&D tax relief scheme, with the merger of the Research and Development Expenditure Credit (RDEC) and Small and Medium-sized Enterprise (SME) schemes as the centrepiece. This merger, scheduled for April 1, 2024, aims to simplify the process of claiming tax relief, making it more accessible for businesses involved in R&D.

- Merger of RDEC and SME schemes: Previously, the RDEC and SME schemes catered to larger and smaller companies, respectively, each with their own set of rules and benefits. However, these schemes have now been amalgamated into a single framework, simplifying the process. This new measure introduces an above-the-line credit that enables companies to claim their qualifying R&D costs. Consolidating these schemes establishes a unified set of rules and criteria, reducing complexity and administrative burdens. It combines the best elements of both relief schemes under a common set of rules, benefiting businesses of all sizes.

- Proposed rates for the merged scheme: The rate offered under the merged scheme will be implemented at the current RDEC rate of 20%. The notional tax rate applied to loss-makers in the merged scheme will be the small profits rate of 19% rather than the 25% main rate set in the current RDEC.

- Introduction of the SME-intensive scheme: A new SME-intensive scheme is being introduced alongside the merger. This scheme lowers the originally proposed threshold for qualifying as R&D intensive from 40% to 30% of total expenditure. This adjustment broadens eligibility, allowing more SMEs, around 5,000, to qualify for enhanced support if a significant portion of their expenditure is dedicated to R&D.

Additional details about the merged scheme

- Contracted-out R&D: Eligibility for contracted-out R&D has significantly changed. There had been proposed restrictions on claiming relief for subcontracted R&D, especially under the SME scheme. Now, the company that initiates, manages, and bears the risks of an R&D project can claim relief for contracted tasks. This change ensures that the primary innovator can access tax relief, whether performing all R&D activities or outsourcing some. It aligns the relief more closely with entities genuinely driving and investing in R&D, simplifying the process and providing more support for innovation.

- Rules for subcontracting: Companies can claim costs for contracted R&D work, but subcontractors delivering project outcomes for another company’s project cannot claim for the same activities. This distinction aims to prevent double claims and streamline the claiming process.

- Treatment of subsidised expenditure: The new scheme modifies the rules regarding subsidised expenditure. If grants or other sources partially fund a company’s R&D, this will not reduce the support available under the merged scheme, simplifying the claiming process.

- Externally Provided Workers (EPWs): The new legislation will clarify the treatment of EPWs, focusing on removing overseas expenditure.

- Step 2 Reduction for Loss-Makers: The merged R&D tax relief scheme aligns benefits for loss-making companies with those of profit-makers. It allows companies to offset the reduced amount against future tax liabilities. The net benefit at Step 2 is calculated using the taxpayer’s applicable tax rate: the small profits rate (SPR) at 19% or the main rate at 25%, with the SPR, specifically applied to loss-makers. This change ensures that loss-making companies receive a more substantial upfront cash benefit than the previous position set out in July.

- Commencement and transition: These changes will take effect for accounting periods starting on or after April 1, 2024, giving businesses time to adapt to the new system. For RDEC claimants, this represents a delay compared to the draft legislation, allowing for a smoother transition.

Navigating New R&D Tax Relief Changes

Implementing new reforms in R&D tax relief schemes marks a transitional phase for businesses. Adapting to these changes can be challenging, particularly in ensuring that processes align with the updated regulations. In this dynamic landscape, it is crucial for businesses to review and adjust their strategies to ensure compliant and optimised claims.

At EmpowerRD, we are dedicated to guiding you through these changes, ensuring that your claims are both compliant and optimised. If you have any questions, please don’t hesitate to contact us today. We’ll also have an upcoming podcast on the impact of the Autumn Statement on innovation and R&D tax relief, which will be available to listen to on the 22nd of November.

Additional support measures in the Autumn Statement

The Autumn Statement extends beyond R&D tax relief reforms. The permanent establishment of full expensing for plant and machinery investments complements R&D investment by reducing capital costs. Additionally, £4.5 billion allocated to strategic manufacturing sectors like auto, aerospace, life sciences, and clean energy from 2025 enhances the potential for R&D activities in these industries.

Impact on university spin-outs and early-stage companies

The government’s endorsement of the Independent Review of Spin-outs is critical in supporting university research and its commercial applications. Furthermore, the extension of the Enterprise Investment Scheme (EIS) and Venture Capital Trusts (VCT) until 2035 ensures that startups and SMEs continue to have access to essential growth capital, fostering a vibrant ecosystem for innovative early-stage companies.

Future outlook for R&D in the UK

The Autumn Statement for 2023 paints a promising picture for the UK’s R&D sector. The combination of financial support and structural reforms is poised to elevate the country’s status as a global leader in innovation and technology. The increased investment and simplified tax relief process promise to accelerate growth and development in various sectors, making the UK an even more attractive location for R&D activities.

Conclusion

The Autumn Statement for 2023 represents a significant step forward in supporting and stimulating R&D in the UK. The R&D tax relief reforms and additional support measures signal the government’s strong long-term commitment to innovation and technological advancement. For R&D tax credit providers and their clients, these changes open new avenues for exploration, funding, and growth, ensuring that the UK remains at the forefront of scientific and technological innovation.

References:

“Technical note on changes to R&D tax reliefs at Autumn Statement 2023”: Details the reforms to R&D reliefs from April 2024, including the merged RDEC and SME intensives scheme and changes in policies for contracted R&D and subsidies

“Merger of SME and RDEC schemes”: Describes the combination of the current RDEC and SME R&D relief schemes into a merged scheme, outlining new rates, tax treatments, and policy objectives

“Autumn Statement 2023”: The broader document from HM Treasury presenting the UK government’s fiscal policies for 2023