HMRC’s latest R&D tax credit statistics for 2025 reveal a mixed picture. The total number of claims has dropped sharply, yet UK businesses are still spending heavily on R&D.

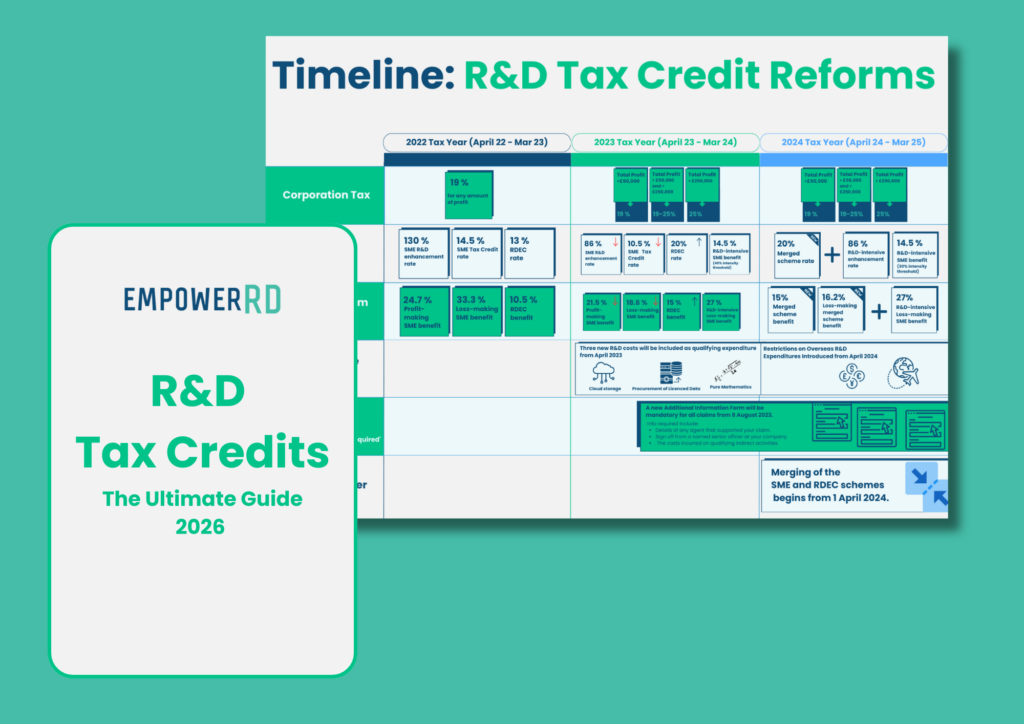

The statistics cover the 2023-24 year, which marks the first full year impacted by the April 2023 rate reforms and the introduction of the Additional Information Form (AIF). These measures have strengthened compliance, but they’ve also raised new barriers for SMEs that innovate.

Claim numbers continue to fall

- 46,950 total claims in 2023–24, which is down 26% from the previous year.

- SME scheme: 36,885 claims (-31%)

- RDEC scheme: 10,065 claims (-5%)

This is the second consecutive year of steep decline. In just two years, the number of companies claiming has effectively halved.

Rob Whiteside, CEO of EmpowerRD, said:

“These statistics show progress and challenge. Fraud and error have been cut significantly, which is good news for the scheme’s integrity. But participation is falling fast; overall claims dropped by 26% last year, and SME claims by nearly a third. That tells us UK businesses are still spending on innovation, but fewer are able to access the support they’re entitled to.”

Total R&D tax credit claims

Hover over each bar to see more insight.

The Integrity Scorecard

The compliance reset has not just reduced fraud; it has also proven highly effective in enforcement. HMRC data shows its intensified scrutiny is working:

- £441 Million Identified: HMRC identified £441 million in incorrectly claimed relief through compliance checks in the 2023-24 year.

- Enforcement Success: Compliance coverage increased to 17% of claims (up from 10% the previous year), and 77% of all checked claims required an adjustment.

While these figures validate the scheme’s improved integrity, they also highlight the significant administrative risk now facing all applicants, underscoring the shift in HMRC’s approach from passive relief provider to active enforcer.

Smaller claims squeezed out

The steepest falls were among claims worth under £15,000, while larger claims over £250,000 proved more resilient. It’s also worth noting that the average claim value increased by 33% compared to last year. This shows how compliance and rate changes are hitting small startups hardest, while bigger companies continue to claim successfully.

Innovation spend remains resilient

Despite fewer claims, the amount of qualifying R&D expenditure is holding steady, with the total at £46.1bn qualifying expenditure (-1% year-on-year). This resilience suggests companies are still investing in R&D, but many are either not claiming or struggling to complete the process.

Hari added:

“On the surface, the headline number looks flat: £7.6bn of support claimed, just 1% down on last year. In reality, I’d expect that figure to rise once HMRC has full visibility of late and amended claims. What is more telling is the mix underneath. For the first time, the value of RDEC claims has overtaken the SME scheme, a direct result of the rate changes. At the same time, total qualifying expenditure is effectively static year-on-year, which shows that UK businesses are continuing to invest in R&D even if fewer are filing claims.”

Who benefits now?

Rate changes have shifted the balance of support:

- SME scheme: £3.15bn claimed (-29%)

- RDEC scheme: £4.41bn claimed (+36%)

For the first time, RDEC overtook the SME scheme in value; reshaping the scheme in favour of larger, more established companies.

A Crucial Lifeline for the R&D Intensive

Although the standard SME scheme was severely cut, a key policy measure offered a reprieve to the most R&D-intensive loss-making companies. The statistics show this targeted approach is reaching the intended beneficiaries:

- 3,990 Companies were successfully identified as R&D Intensive and qualified for the higher 14.5% credit rate, helping to mitigate the full impact of the rate cuts.

This targeted support, alongside the merged scheme and the new Enhanced R&D Intensive Support (ERIS) coming into force, shows a move toward a more selective system focused on rewarding high-risk, high-spend innovators.

Education gap is holding SMEs back

HMRC announced plans in October 2024 to better educate businesses on accessing the R&D scheme. However, little has been implemented since then. Our recent innovation report underscores the need for HMRC to provide more claimant education, revealing that 52% of businesses view regulatory complexity as their biggest barrier to innovation. On top of this, HMRC revealed that over 50% of claimants self-claim without R&D agents.

Hari Sandhu said:

“Businesses are calling out for more support in navigating the scheme. HMRC has already recognised this need, but we’re yet to see meaningful progress. Providing clearer education and guidance would be one of the quickest levers to pull to help stimulate claim volume.”

The disappearing first-time claimant

The challenge is even starker when looking at new businesses. A decade ago, between 2–3% of newly registered companies went on to make a first-time R&D claim each year. In 2023–24, that figure dropped to just 0.42% – the lowest on record.

Rob Whiteside commented:

“It’s stark to see so few new companies getting R&D support. Are today’s founders less innovative, or are they more scared, or unable, to claim? Right now, we are only rewarding success that is already stable, instead of sowing the seeds for the UK to create the next OpenAI. That’s a missed opportunity.”

First-time R&D claimants as % of new companies

Hover over each bar to see more insight.

Regional and sector patterns

- London: 24% of claims / 31% of relief

- South East: 15% / 20%

- East of England: 10% / 13%

- Top three sectors (Info & Comms, Manufacturing, Professional/Scientific/Technical): 71% of relief

These patterns remain consistent year-on-year.

Looking ahead

2023–24 is the last year under the separate SME and RDEC schemes. From April 2024, the merged scheme and Enhanced R&D Intensive Support (ERIS) for loss-making SMEs took effect.

Next year’s statistics will show how these structural reforms reshape the balance once again.

EmpowerRD’s view

Recent cuts to R&D tax relief rates and stricter compliance measures have led to a 31% fall in SME claims and a sharp drop in participation. This directly contradicts the UK Innovation Strategy’s goal to widen access and stimulate private sector innovation. Unless policy is realigned, these reforms risk suffocating the diversity and ambition needed for the UK to become a global leader in innovation.