In our feedback to the draft legislation published on 20 July 2022, we have identified the measures that we think will impede R&D activity and potential growth in the UK.

The first relates to the proposal to refocus qualifying R&D expenditure for subcontractors and externally provided workers towards innovation undertaken in the UK. The second links to HMRC’s measures to help prevent abuse of the R&D scheme.

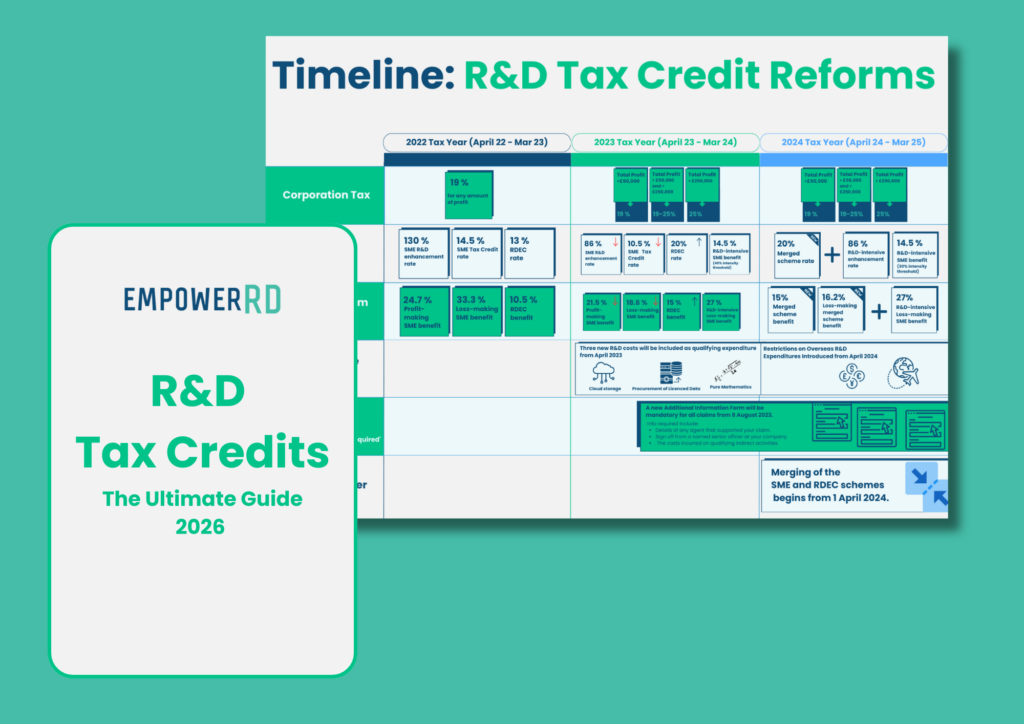

Changes to overseas R&D

By excluding overseas R&D costs, the government is trying to encourage R&D activity in the UK. This change also makes logical sense; including overseas R&D costs goes against the fundamental objectives of the R&D schemes to increase and retain innovation within the UK.

We’re also happy that the government listened to stakeholders and narrowed exemptions for some qualifying overseas expenditures where appropriate conditions do not exist in the UK. For instance, R&D activity will likely qualify when there are material factors like geography, environment, population or other conditions that are not present in the UK but are required for the research.

It’s also worth noting that the UK has been an outlier in allowing overseas costs to be included with the R&D scheme, so this change reflects a similar approach to how the scheme already operates in most other OECD countries.

Push back reform to April 2024

However, it’s important to understand that these changes will have an overwhelming impact on many UK businesses. Estimates from the Office for National Statistics suggest that the proportion of such overseas expenditure within UK R&D claims may be as much as £21.6 billion. This equates to just over 45% of the total £47.5 billion R&D expenditure used to claim tax credits in 2019-20. So the proposed reforms would have a major financial impact on many UK businesses.

This is why we have recommended that the reform is pushed back to after April 2024. This gives businesses time to adapt supply chains and restructure in order to accommodate these proposals.

Clarify qualifying conditions for overseas R&D

We have also recommended that the “lack of a suitable technical skill set in the UK” is listed as a qualifying condition. There are many situations where a UK business may stumble across a challenge that can only be solved by an overseas technical expert.

Provide more detailed guidance

We have also recommended that HMRC publish detailed guidance, as well as the final legislation, on the method of how claimants should claim for overseas costs within the exemption conditions, along with guidance about what supporting records HMRC would expect claimants to hold in order to justify such a claim.

HMRC’s measures to help prevent abuse of the R&D scheme

Overall, we’re pleased with the new proposed measures to help prevent abuse of the R&D tax relief scheme. We did make some additional suggestions.

Claim report signatories

At EmpowerRD, we always put our name on each report submitted, and we welcome the new mandatory requirement to name any advisor who has helped with an R&D claim. It is critical to us that every claim is compliant and optimised, and we’re happy to take responsibility for each one. We hope this change will create more accountability within the R&D adviser market.

Additionally, requiring a senior officer of the company to claimant sign off on the report puts an end to the practice of some R&D advisors not sharing the full report with their clients. This has been an issue for many companies who have switched to us from other providers, so it’s great to see this issue addressed.

Guidance on claim report content

We have recommended that HMRC provide detailed guidance on what is expected to be included in the R&D claim report. We already provide HMRC with a very comprehensive report in support of all our claims and are keen to see HMRC raise the bar market-wide.

Pre-notification for first-time claimants

We assume that the method of pre-notification would be via an easy-to-use digital method, and there would be scope for agents to help clients with this via an API. It would be reassuring to hear that this is the case.

We think pre-notification requirements should be extended to nine months after the period end, rather than the suggested six months. This would allow companies more time to notify, and coincide with the Companies House accounts filing requirements.

Further education

We have also recommended that HMRC make sure to actively spread the word about these significant changes to ensure that claimants are prepared when they take effect.

Next steps

On the 13th of September, we provided feedback on the draft legislation. We’re keen to see the final legislation, which should be published around the same time as the annual Autumn Budget, scheduled to be announced in November. We’ll let you know more as soon as we learn more.

Unsure what this means for your claim?

Contact us to learn more about how these changes may affect you.