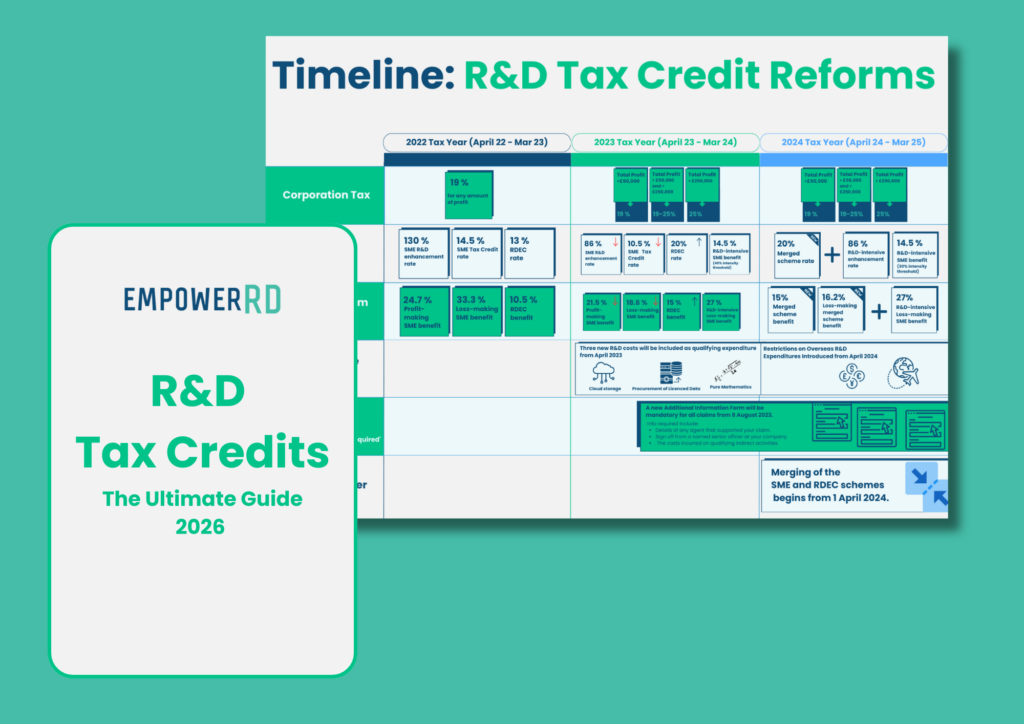

In November 2022, the Autumn Statement announced significant adjustments to UK R&D tax credit rates, which will come into effect on 1 April 2023.

Because these changes are likely to impact your company’s future R&D tax credit claims, it’s important you understand exactly what is changing. That way, you can estimate the potential value of your future claim and plan your company’s finances accordingly.

To help you understand the R&D rate adjustments, we’ve created a quick reference guide with examples that address various circumstances. Whether you’re a loss-making or profitable SME or a large company claiming through the RDEC scheme, we’ve covered you. Download your free guide to get up to speed now.

We’ve also included a brief overview of the upcoming changes in tax relief rates, along with examples for context.

Main changes to the R&D tax credit scheme

The SME Scheme will become less generous starting from April 2023

To improve compliance and combat fraud and error, the government is reducing the scheme’s benefits for Small and Medium-sized Enterprises (SMEs). The enhanced R&D expenditure rate for SMEs decreases from 130% to 86%, and the SME tax credit rate will reduce from 14.5% to 10%.

Most loss-making SMEs currently receive up to 33% payable credit on qualifying R&D expenditure, but from 1 April 2023, it will reduce to 19%. And for most profit-making SMEs, the effective net tax benefit of R&D tax relief will reduce from 25% to 22%.

Example of a loss-making SME with an accounting period beginning on 1 April 2023

Below is a calculation for a loss-making SME claiming through the SME scheme with an accounting period starting on 1 April 2023 and ending on 31 March 2024. The company’s total qualifying R&D Expenditure (TQE) is £1,000,000.

Calculation

Total Qualifying R&D Expenditure (TQE) x enhanced expenditure rate

£1,000,000 x 86% = £860,000

Maximum surrenderable loss (186%)

(£1,000,000 + £860,000) x 10% = £186,000

TAX CREDIT CLAIM VALUE: £186,000

The Research and Development Expenditure Credit (RDEC) Scheme will become more generous starting from April 2023

According to government research, the RDEC scheme is a stronger investment for taxpayer money as it creates more economic value. For this reason, the rate of the RDEC will grow from 13% to 20%. That’s a 42% increase in generosity (after tax) from 10.5% to 15%.

Example of an RDEC claim with an accounting period beginning on 1 April 2023

Below displays the calculation for a company claiming through the RDEC scheme with an accounting period starting on 1 April 2023 and ending on 31 March 2024. The company’s total qualifying R&D Expenditure (TQE) is £1,000,000. Corporation tax will increase from 19% to 25% in April 2023 for most companies, so this information is also included below.

Calculation

Total Qualifying R&D Expenditure (TQE) x New RDEC Rate

£1,000,000 x 20% = £200,000

Gross Credit Amount – New Corporation Tax

£200,000 – 25% = £150,000

TAX CREDIT CLAIM VALUE: £150,000

If my accounting period falls during the changeover between old and new R&D tax rates, what happens?

If your year-end date is not 31 March, you will need to do a split period calculation for R&D costs to correctly apply the rates of relief.

For instance, if your accounting period starts on 1 October 22′ and ends on 30 September ’23, you will need to apply the old rates to the first half of the year (182 days up to 31 March) and then the new rate to the second half of the year (183 days up to 30 September).

To see detailed examples of split calculations with old and new rates for both the SME and RDEC scheme, download our quick reference guide below.

Download your free quick reference guide now!